Grahamian Value Week in Review ― September 18, 2020

Grahamian Value Week in Review ― September 18, 2020

“If everything you do needs to work on a three-year time horizon, then you’re competing against a lot of people. But if you’re willing to invest on a seven-year time horizon, you’re now competing against a fraction of those people, because very few companies are willing to do that.”

― Jeff Bezos (2011)

PART ONE.

WEEK IN REVIEW

PART TWO.

FURTHER RESOURCES

In the past week —

We have added historical balance sheet data to all Grahamian Value listed company profiles.

I. WEEK IN REVIEW

Recent developments at two Grahamian Value listed companies companies grabbed the eye of the co-editors; and one company, more generally, stands out as deserving of further exploration.

Monday’s tweet grabbed our eye and spurred our deeper look into Rubicon Technology:

Bandera Partners (note: see also Tandy Leather) amended their ownership filing in Rubicon Technology to reflect larger ownership due to a reduced number of company shares outstanding. Rubicon Technology’s share count totaled 2,472,393 as of June 30, 2020 (compared to 2,702,171 as of December 31, 2019) with corporate repurchase activity detailed below:

The company’s most recent 10-Q filing notes, “As of August 3, 2020, the Registrant had 2,406,225 shares of common stock” — meaning, a further reduction of 66,168 shares since June 30, 2020. We’re intrigued to see Rubicon Technology’s share count decline by nearly 11% (so far) this year.

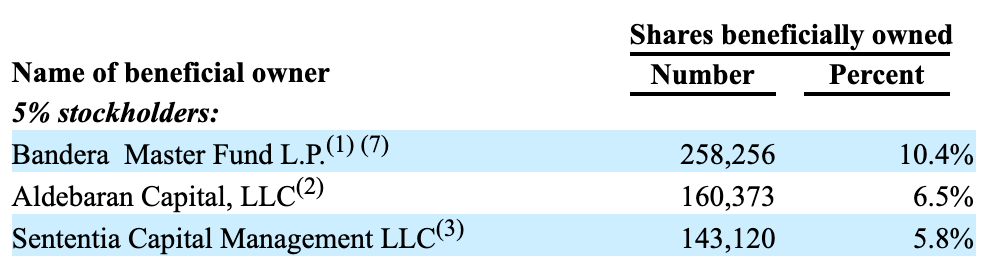

Rubicon Technology is a “perennial” net-net, the full list of beneficial owners is interesting:

Aldebaran Capital — Form SC 13D, filed June 30, 2017

“We share a simple, yet rarely practiced investment discipline that derives from the work of Benjamin Graham and his classic textbook Security Analysis (1934).”

Ken Skarbeck is President and Managing Partner.

Ed Skarbeck is Vice President and Managing Partner.

Sententia Capital Management — Form SC 13D, filed December 4, 2017

“Sententia is a value investing based capital management firm that runs a concentrated, deep value portfolio.”

Michael Zapata, a former Navy SEAL and graduate of Columbia University's Heilbrunn Center for Graham & Dodd Value Investing Program, is the founder of Sententia Capital Management.

As described by Mario Gabelli, “[Mr. Zapata] was highly successful in his former profession. He has the intangibles of great investors and he is proving to be a great investor in the tradition of Graham and Dodd.”

Mr. Zapata explains his journey, below —

The co-editors are grateful to Dave Sather of Sather Financial Group in Victoria, Texas for bridging the above conversation.

(Full Disclosure: the co-editors are personal shareholders in Schmitt Industries, a publicly-traded business for which Mr. Zapata serves as both Chairman and CEO. Additionally, the co-editors personally own shares in Rubicon Technology and Dawson Geophysical Co.)

The tweet below caught our attention regarding Mammoth Energy, the business on the GV | United States list with the steepest discount between public market valuation and net current asset value. Importantly, net current asset value is comprised almost entirely of accounts receivable, which may be doubtful given the state of the underlying industry.

Watching the behavior of company insiders can be informative —

Arthur Smith sold a block of 6,000 shares on December 2, 2018 at an average price of about $24.85, as detailed in this SEC Form 4 filing. As suggested by this chart, Mr. Smith’s exit in late 2018 was particularly well-timed.

We’re intrigued to see Mr. Smith (with personal cash outlay) increase his personal ownership in Mammoth Energy Services by 20,000 shares. Prior to his open-market purchase, Mr. Smith held just under 110,000 shares obtained primarily through stock grants received as a company director, where he serves as Chair of the Audit Committee.

Per below, Dawson Geophysical Co. recently captured Harry’s attention:

And in more than 140 characters —

II. FURTHER RESOURCES

Harry Sauers, co-editor of Grahamian Value, on Dawson Geophysical Co.

I’ve been taking a closer look at Dawson Geophysical Co., a business that I discovered via the GV | United States weekly list. Dawson is a seismic data firm, providing information about the contents of the earth’s crust to data libraries, who in turn sell the information to oil and gas companies.

Dawson is particularly interesting since it trades at a discount to its net current asset value (most of which is cash) yet is both GAAP net income and free cash flow positive for the first half of 2020, a period marked by major distress and a number of bankruptcies across the energy sector. Dawson, like many other cyclicals, was previously valued on its cash flow rather than assets, and now is priced for disaster — at valuations generally reserved for seriously distressed companies or those facing imminent disruption of revenues.

Based upon Dawson’s strong balance sheet liquidity and the cyclical nature of the industry, neither of these factors appears to be true, suggesting that the market may have thrown the baby out with the energy stock bathwater. While I’m typically cautious regarding net-net situations in the energy sector, Dawson nonetheless warranted a deeper look.

History

Dawson Geophysical was founded in 1952 and has survived a number of industry booms and busts. The large cash position and credit availability maintained throughout COVID-19 was a wise move and ensured that the company would be well-positioned emerging from the crisis to take advantage of an eventual rebound in demand for seismic data services while its competitors, notably Geokinetics and SAExploration Holdings (side-point here) have both filed for bankruptcy in the past two years.

While the oil and gas industry, and by extension seismic data providers, have been decimated, Dawson is structurally-sound and has limited risk of impending liquidity issues, and has no debt. Additionally, Dawson’s pivot to serving primarily multi-client data libraries, as opposed to oil and gas firms themselves, diversifies risks to demand while providing a credit-buffer between Dawson and potentially distressed customers.

Findings

The company has been profitable in the first half of 2020, a bit of an anomaly for the industry — it seemed likely that Dawson is doing something truly unique as a company, especially given the large base of institutional owners — including 10% owner Gate City Capital, an investment firm based in Chicago founded by Michael Melby, whom I respect and admire. Employee reviews on Glassdoor seem to confirm the operating uniqueness of Dawson: every employee review approves of Chairman and CEO Stephen Jumper, and many discuss how Dawson is doing a fantastic job despite the challenges of operating in a cyclical industry.

Other companies in this space have proven themselves to be similarly profitable over full business cycles — such as TGS (written up on Value Investors Club by finn520 on July 16, 2010 and by flux13 on July 18, 2014) and Pulse Seismic, of which Bob Robotti, another investor I particularly admire with deep expertise in cyclical energy stocks, is the Chairman of the Board of Directors. Energy is by nature cyclical; companies likely to survive the down-cycle, such as Dawson, are positioned to benefit from the rebound.

With these factors piquing my interest in Dawson, I set out to dig through Dawson’s SEC filings to figure out the reasons behind the beaten-down valuation. In my research, I noticed that depreciation and amortization charges ($9.29 million in just the first half of 2020) were well in excess of Dawson’s necessary capital expenditures of $5 million per year. Deeper research revealed that Dawson had over-invested in PP&E until late 2014, thus requiring accounting charges against net income that had no effect on actual cash outlays.

Dawson managed to generate over $3 million in free cash flow in H1 2020 on $68.4 million in revenues, while recognizing $11.6 million in EBITDA and spending just $2.76 million on capex. For a period that by all accounts ought to be close to the cyclical trough, these are very impressive results and I believe that FCF will more closely approximate EBITDA minus capex as accounts receivable are converted into cash.

Attempting to normalize Dawson’s earnings power over a full cycle requires a series of assumptions. Dawson’s average revenues from 2014 thru 2019 (which were in a downtrend, already) are $165.6 million and Dawson generated EBITDA margins of 16.9% in H1 2020, suggesting that normalized EBITDA is somewhere around $28 million per year. Based upon management’s stated $5 million maintenance capex, Dawson Geophysical’s normalized earnings power is about $23 million before taxes and currency adjustments.

Valuation

Dawson has quite a bit of excess cash and no long-term debt, which is a radically different capital structure from operating peers. In valuing Dawson’s earnings, the enterprise value metric is most appropriate, to best remain agnostic to the capital structure and assess the price that a would-be acquirer would pay for Dawson Geophysical.

Dawson has $31.8 million in cash and equivalents, $5 million in restricted cash, $5.5 million in long term leases, and no debt. The current market cap of DWSN stock is around $38 million, for a total enterprise value around $7 million. Regardless of one’s approach, less than 0.5x EV/EBITDA - capex during an economic trough is extraordinarily cheap.

This factor is not appreciated by the market, likely due to the excess depreciation and amortization charges that Dawson must take against net income, even though they are not cash outlays nor are they representative of Dawson’s maintenance capital expenditure needs.

From a liquidation standpoint, Dawson trades at a material discount to net current assets, which are mostly in cash and the remainder almost entirely in receivables. Dawson has a line of credit with Dominion Bank, which has agreed to extend credit to Dawson up to the lesser of $15 million or 80% of receivables. It is reasonable to assume that a bank is better equipped to underwrite these receivables than we are, so taking net cash plus receivables at 80% leaves a conservative estimate of liquidation value of $1.81 per share.

The full research report on Dawson Geophysical is available on Seeking Alpha here: Dawson Geophysical: Outrageous Value And Repurchase Opportunity.

For Grahamian Value readers: key calculations, additional resources, and primary source data are accessible via a private data room. If you’d like access, please contact the co-editors at grahamianvalue@gmail.com

ABOUT GRAHAMIAN VALUE

Founded in 2020, Grahamian Value is a labor of love centered around our desire to openly share data and perspectives that we find helpful in our pursuit of Benjamin Graham-inspired investment ideas.

The co-editors of Grahamian Value, as of the date of this communication, may individually own shares of companies mentioned herein. The publishers do not receive compensation from the companies and people covered in Grahamian Value for such coverage. This communication is for informational purposes only. This is not intended to be investment advice. Seek a duly licensed professional for investment advice.