Grahamian Value Week in Review ― October 9, 2020

Grahamian Value Week in Review ― October 9, 2020

“Ick investing” means taking a special analytical interest in stocks that inspire a first reaction of “ick.” I tend to become interested in stocks that by their very names or circumstances inspire unwillingness — and an “ick” accompanied by a wrinkle of the nose on the part of most investors to delve any further.

― Dr. Michael Burry, October 2001

PART ONE.

WEEK IN REVIEW

PART TWO.

WEEKEND READING

In the past week —

One new business has been added to the Grahamian Value list of companies.

We’ve observed notable developments at two Grahamian Value listed companies.

I. WEEK IN REVIEW

Newpark Resources, Inc. is a new addition to the GV | United States list.

Newpark Resources, Inc. is a worldwide provider of value-added fluids and chemistry solutions in the oilfield, and engineered worksite and access solutions used in various commercial markets. (source)

The prior Week in Review noted the extraordinary decline of market capitalization at Now Inc., a worldwide supplier of energy and industrial products and engineered equipment solutions:

Oil and gas markets are incredibly distressed, driving a dislocation in sector market valuations. Now Inc.’s market capitalization peaked in 2014 at roughly $4 billion and has since declined by more than 85%... — Grahamian Value Week in Review (October 2, 2020)

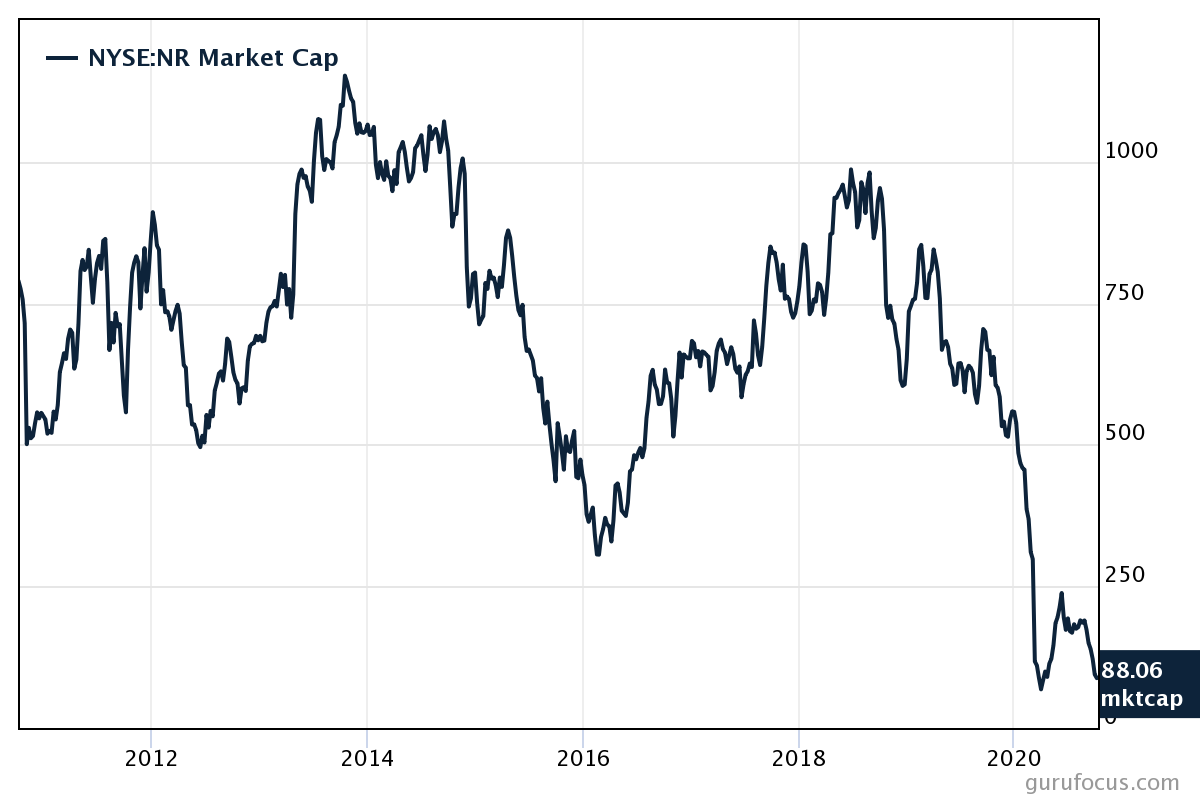

This week’s new addition is more of the same; the market capitalization of Newpark Resources is down over 90% from the not-too-distant peak(s) of $1 billion —

With this decimation of market value, Newpark Resources is valued below (unadjusted) net current assets. Per the company’s most recent 10-Q, net current assets (unadjusted) as of June 30 totaled slightly more than $100 million or just over $1.10 per share: $43 million of cash and cash equivalents, plus $140 million of net receivables, plus $178 million of net inventories, plus $21 million of prepaid expenses and other current assets, less $11 million in current debt, less $52 million of accounts payables, less $33 million in accrued expenses, less $125 million in long-term debt, and less $58 million in assorted other liabilities. As of July 31, 2020, a total of 90.6 million shares of common stock were outstanding.

As detailed in the 10-K:

Newpark Resources, Inc. was organized in 1932 as a Nevada corporation. In 1991, we changed our state of incorporation to Delaware. We are a geographically diversified supplier providing products, as well as rentals and services primarily to the oil and natural gas exploration and production (“E&P”) industry. We operate our business through two reportable segments: Fluids Systems and Mats and Integrated Services. Our Fluids Systems segment provides customized drilling, completion, and stimulation fluids solutions to E&P customers primarily in North America and Europe, the Middle East and Africa, as well as certain countries in Asia Pacific and Latin America. Our Mats and Integrated Services segment provides composite mat rentals utilized for temporary worksite access, along with related site construction services to customers in various markets including E&P, electrical transmission & distribution, pipeline, solar, petrochemical, and construction industries across North America and Europe. We also sell composite mats to customers around the world.

With regards to the Fluids Systems segment:

Our customers are principally major integrated and independent oil and natural gas E&P companies operating in the markets that we serve. During 2019, approximately 53% of segment revenues were derived from the 20 largest segment customers. No single customer accounted for more than 10% of our segment revenues.

And, regarding the Mats and Integrated Services segment:

Our customers are principally oil and natural gas E&P companies, utility companies, and infrastructure construction companies operating in the markets that we serve. During 2019, approximately 55% of our segment revenues were derived from the 20 largest segment customers. No single customer accounted for more than 10% of our segment revenues. The segment also generated 92% of its revenues domestically during 2019. As a result of our efforts to expand beyond our traditional E&P customer base, revenues from non-E&P markets represented approximately 55% of our total segment revenues in 2019.

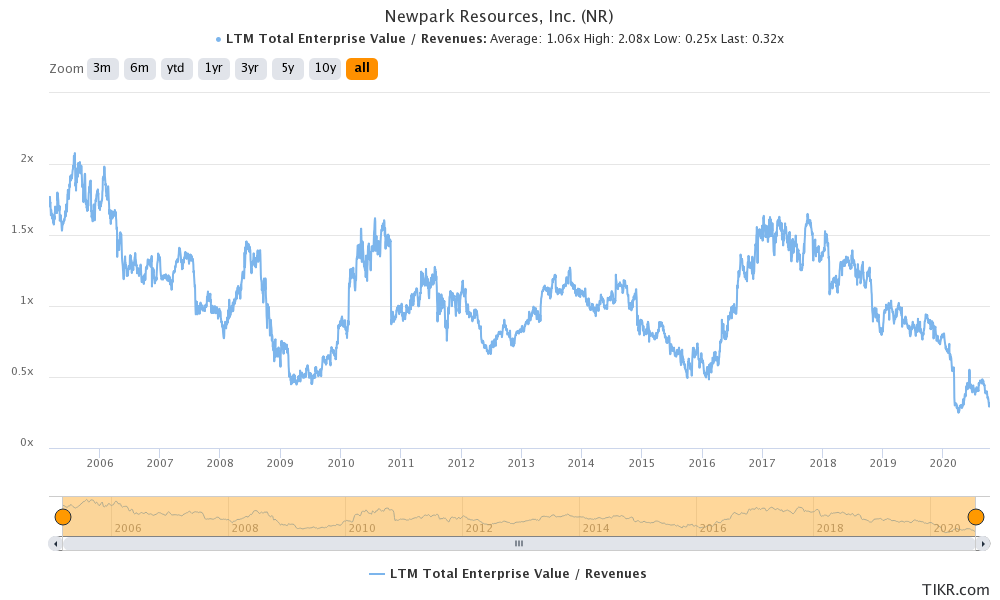

With prior EBITDA margins in the 10%, (and higher) range, Newpark Resources is currently priced at 0.3x Enterprise Value to Revenue. Momentary valuations are meaningfully lower than those observed in both the abyss of 2009 and the 2016 energy bust —

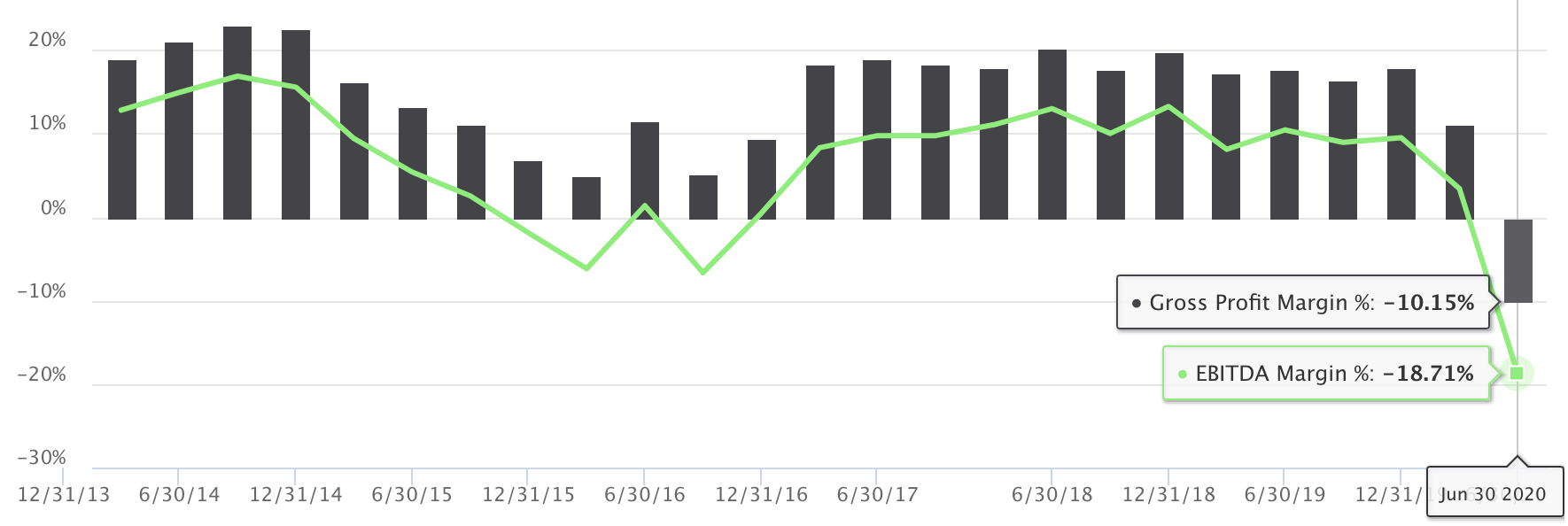

This time, however, is different. Presently, Newport Resources faces negative gross margins and EBITDA margins are at all-time lows —

As would be expected, the company is aggressively cutting costs, as detailed in the 10-Q filed with the SEC on August 4, 2020:

We have taken a number of actions aimed at conserving cash and protecting our liquidity, including workforce and salary reductions, elimination of all non-critical capital expenditures, as well as actions to reduce our operational footprint to match current and anticipated activity levels by operating region. We currently expect total 2020 capital expenditures to be approximately $15 million.

Against this backdrop of $15 million of anticipated annual capital expenditure, the company allocated (as of June 30) slightly over $33 million for the repurchase of convertible notes at a $4 million discount to par value; the company’s securities repurchase program maintains a $51.9 million authorization. Also, in the midst of the COVID-19 uncertainties, the company implemented a poison pill (for anti-takeover purposes, we conjecture).

In contrast to other companies we’ve explored to date, Newpark Resources maintains a substantial amount of long-term debt (offset by current net receivables and inventories). The recent repurchase of discounted convertible notes (from our outside view) appears a solid move; we commend the Board for the opportunism.

Update: Hudson Global, Inc.

On October 1, 2020, Hudson Global, Inc. announced the acquisition of Coit Group, another recruitment process outsourcing (RPO) company:

Founded 20 years ago by Joe Belluomini and Tim Farrelly, Coit is an RPO provider specializing in procuring top talent for high-growth companies, predominately in the San Francisco Bay Area. With this acquisition, Hudson RPO significantly expands its presence in the technology sector and establishes an office in San Francisco. In addition, Joe Belluomini and Tim Farrelly will become co-CEOs of Hudson RPO’s newly-formed Technology Group. (source)

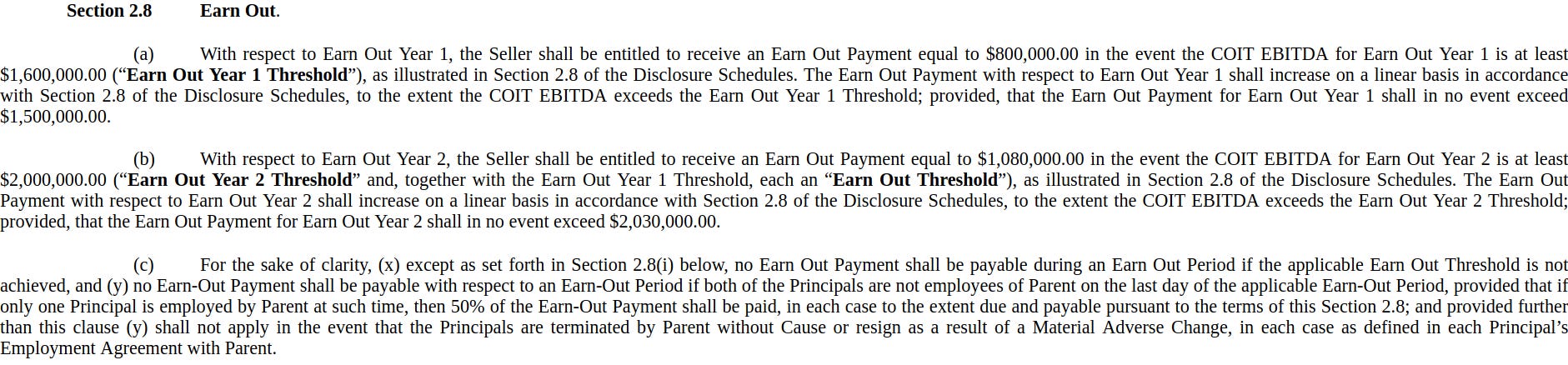

While we lack any financials on Coit Group, we’ve taken notice of the particular financing agreement of the transaction. As detailed in the asset purchase agreement, Hudson will pay $4 million in cash, a $1.35 million promissory note, assume various liabilities of Coit, and issue $500,000 of Hudson Global stock. Additionally, there is a provision for additional earn-out payments, determined by the EBITDA generated by the acquired business over the next two years —

We are intrigued by the these financing and incentive terms, which warrant a closer look once financial details of the acquired entity become available.

As a “perennial” net-net, Hudson Global itself is a familiar name and has twice been the subject of Value Investors Club write-ups.

March 19, 2018 — Gocanucks97 explored Hudson Global as a “slow liquidation play” while also considering the possibility of NOL monetization through M&A.

May 3, 2017 — Kruger explored a valuation of the company against that of peers while noting the large balance of NOLs, both domestic and international.

This week’s development definitively clarifies a key point of prior uncertainty: a strategy of acquisition and the monetization of NOLs (rather than liquidation and distribution) will drive forward returns at Hudson Global.

Update In Brief: Universal Stainless & Alloy Products, Inc.

Universal Stainless & Alloy Products announced in a press release on October 6, 2020 that the company has:

…reached a new 5-year collective bargaining agreement with the hourly employees at its Titusville, PA facility.

The new 5-year collective bargaining agreement has been ratified by the bargaining unit and is effective as of October 1, 2020. The new contract maintains the flexible work rule terms and profit sharing incentives contained in the prior agreement.

Dennis Oates, Chairman, President and Chief Executive Officer, commented: “We are pleased that the new labor agreement at our Titusville facility allows us to be competitive in the marketplace and attract skilled employees, while being in the best interests of our employees, customers and shareholders.”

(Full Disclosure: the co-editors are personal shareholders in Now Inc., Hudson Global, Inc., and Universal Stainless & Alloy Products, Inc.)

II. WEEKEND READING

“Ben [Graham] would have, of course, been comfortable with Baron Rothschild’s summary of a lifetime’s learning: ‘Buy assets; sell earnings.’”

— Charles D. Ellis, “Ben Graham: Ideas as Mementos” (Financial Analysts Journal, 1982)

Below, the co-editors are proud to share three mini-case studies on this central theme:

i. Bruce Kovner and Edward O. Thorp [full essay]

Jerry Baesel and I spent an afternoon with Bruce [Kovner] in the 1980s in his Manhattan luxury apartment discussing how he thinks and how he gets his edge in the markets. Kovner is a generalist, who sees connections before others do.

About this time he observed that large oil tankers were in such oversupply that the older ones were selling for little more than scrap value. Kovner formed a partnership to buy one. I was one of the limited partners. Here was an interesting hedge. We were partially protected against loss on the downside because we could always sell the tanker for scrap. But we had a substantial upside: Historically, the demand for tankers had fluctuated widely and so had their price. Within a few years, our refurbished 475,000 ton monster, the Empress Des Mers, was profitably plying the world’s sea lanes stuffed with oil.

ii. James S. Tisch [full speech]

Let’s go back to 1975, when there was a building boom in supertankers, brought about by relatively low oil prices that had caused large increases in oil demand. A few years later, in the late ‘70s, there was an oil embargo and resulting oil price hike, which drastically reduced the amount of oil coming out of the Persian Gulf – much less oil, but still lots of tankers, now just bobbing in the water. It was soon afterward, in the early ‘80s, that we started thinking about buying tankers. We had seen from reading newspapers that the worldwide supply of tankers was vastly overbuilt; according to quoted estimates, the market required only 30% of the ships that were afloat. As a result, ships were trading at scrap value. That’s right. Perfectly good seven-year-old ships were selling like hamburger meat – dollars per pound of steel on the ship. Or, to put it another way, one was able to buy fabricated steel for the price of scrap steel. We had confidence that with continued scrapping of ships and increased oil demand, one day the remaining ships would be worth far more than their value as scrap. We were sure of three other things: First, by buying at scrap value, there was very little downside. Second, we knew that the ships would not rust away while we waited for the cyclical market to turn. And third, we knew that no one would build more ships with existing ships selling at a 90% discount to the new build cost. We were confident that the demand for oil, particularly from the Persian Gulf, would ultimately increase with worldwide economic growth and so the remaining tankers would ultimately be worth much more than their scrap value.

So we did the logical thing -- we took out the yellow pages, looked under “Brokers – Tankers” and from there, made our way to Scotland to get a first hand look and “kick the tires” of some of these big ships that are almost four football fields long. And on board one of these massive vessels was formulated the Jim Tisch $5 Million Test. And what is the Jim Tisch $5 Million Test, you may ask? While on the ship you look to the front and then you look to the rear – then take a look to the right and then to the left –then you scratch your head and say to yourself – “Gee! You mean you get all this for $5 million?!” Just to give you some perspective, these ships, capable of hauling 2-3 million barrels of oil, had been built eight years earlier for a cost of over $50 million.

In all, we purchased six tankers in the early 80’s, all by using the Jim Tisch $5 Million Test. By 1990, the market had turned, as – you guessed it – too many ships were scrapped and the volume of oil coming out of the Persian Gulf increased. And, as good capitalists, when this happened we sold a 50 percent interest in our ships for 10 times the valuation of our initial investment.

Fast-forward to 1997 when opportunity knocked again. We witnessed a set of conditions similar to those of the mid-‘70s – little construction of new oil tankers despite increased production of oil from the Persian Gulf.

That year we decided to build four new ships in reaction to the distinct lack of new building. We sold those ships about a year and a half ago – relying on the same principles applied as before, except in reverse. Oil prices were going up, but then, so was the supply of ships. We could sense that the increased prices for oil would negatively affect demand for oil, and ultimately ships, and therefore bring down the value of our ships. We sold -- probably a year too soon -- but in this business, I would prefer to be early rather than late.

In 1988 we saw a similar situation develop in a related industry -- offshore drilling. In the 80’s, offshore drilling rigs had declined in value dramatically as oil and gas prices were relatively low and worldwide hydrocarbon reserves were flush. But we saw that the demand for oil and natural gas was increasing as a result of these lower product prices. We knew that the demand for rigs would return, and we knew that – like the tankers before them – the rigs would not rust away in the interim.

So we took a trip to the Gulf of Mexico where we went aboard a jack-up oil rig and, yes, we applied the Jim Tisch $5 Million Dollar Test. Remember? You look to front – you look to the back -- you know the rest. A few weeks later, we had bought an offshore rig company named Diamond M, and became the proud owners of 10 drilling rigs for a total investment of about $50 million.

A few years later, with the business still bouncing along the bottom, we bought another offshore oil drilling company, Odeco, which increased our investment in the rig business tenfold, moving us from a $50 million investment to an investment worth $500 million. We renamed the company Diamond Offshore.

By 1995, the cyclical drilling market had changed, and we were making some money in the business. So, as good capitalists, we took the company public where we were able to get all of our money back from our initial investment and still retain a 55 percent stake in the company…

Oil drilling – like tankers — is a cyclical business. Our rigs are contracted by oil companies who pay a day rate which is determined by the supply and demand for oil rigs. An oil rig takes at least three years to build, so the supply of these rigs is relatively fixed over the short-to-intermediate term. However, the demand for rigs can gyrate wildly based on the temperament of oil company managements in response to oil prices, world events, and other factors. Day rates can go up or down by a factor of five or more, just as we’ve seen in the past year and a half. Whereas in mid-2004 we 13 contracted a jack-up rig at $27,000 per day, today that same rig commands over $100,000 per day. We got into the business because we believed the rig assets were undervalued. Over time, we were willing to ride out some very lean years, patiently waiting for the turnaround and humming the Ruby and the Romantics standard, “Our Day Will Come.”

iii. Steven Romick [full letter]

Capital intensive, cyclical businesses often trade at discounts to the value of the underlying assets when their respective industry is in distress (companies are either losing money or earning less than what’s expected in a more normal environment). When earnings rebound, the market seems to forget that the businesses are cyclical. Investors begin to value them on earnings as if another downturn isn’t in the cards. Our average cost in Ensco reflects rigs purchased at a discount to a fully depreciated replacement value. Since then, its stock price has increased, along with day rates (and earnings). The company is now beginning to be considered more on a P/E basis, while at the same time, the value of the underlying rigs has begun to trade through their replacement value, reflecting the value of existing contracts and hope for a continued robust demand environment. As our margin of safety has declined, we have reduced our exposure, consistent with our initial thesis and the manner in which we invest in such industries.

ABOUT GRAHAMIAN VALUE

Founded in 2020, Grahamian Value is a labor of love centered around our desire to openly share data and perspectives that we find helpful in our pursuit of Benjamin Graham-inspired investment ideas.

The co-editors of Grahamian Value, as of the date of this communication, may individually own shares of companies mentioned herein. The publishers do not receive compensation from the companies and people covered in Grahamian Value for such coverage. This communication is for informational purposes only. This is not intended to be investment advice. Seek a duly licensed professional for investment advice.