Grahamian Value Week in Review ― November 13, 2020

Grahamian Value Week in Review ― November 13, 2020

“[Richard] Rainwater always looked for a big event. A blowup in energy prices…then he looked for a powerful way to exploit the upheaval, not just to bet the trend but to turbocharge the bet. To snatch up drilling assets at panic-sale prices and hand them to the oil patch’s most astute operator…he always wanted to find something sick…and then he was generally very knowledgeable in figuring out if he could fix it. He didn’t want anything just undervalued. He wanted it undervalued with an opportunity attached to it. He wanted the guy he was negotiating with to be pretty beat up. Rainwater had a keen instinct for the big picture. He’d identify his idea and put the right CEO in place. ‘Find the guy’, Rainwater preached. ‘Don’t try to be the guy.’”

— Kenneth A. Hersh (2011)

PART ONE.

WEEK IN REVIEW

PART TWO.

AN OPEN CALL FOR READER ASSISTANCE

PART THREE.

FEATURED GUEST INSIGHT

PART FOUR.

WEEKEND WATCHING

PART FIVE.

WEEKEND LISTENING

In the past week —

No new businesses have been added to the Grahamian Value list of companies.

We’ve noticed interesting developments at two Grahamian Value listed companies.

BRIEF OVERVIEW —

Amid the oil and gas carnage, the October 26, 2020 merger of Contango Oil & Gas Company (MCF) and Mid-Con Energy Partners (MCEP) is particularly intriguing. As many readers will likely notice, this is our fifth consecutive week with no material change in the list of GV | United States companies.

I. WEEK IN REVIEW

Changes in Beneficial Ownership: Newpark Resources, Inc.

First explored in our October 9, 2020 Week in Review, Newpark Resources is now removed from the S&P SmallCap 600 index. The co-editors surmise that de-indexation is a (partial) driver of recent institutional shareholder activity —

SC 13G/A filed by Blackrock (November 9, 2020)

Documents beneficial ownership of 6,833,408 shares (7.5% of shares outstanding), down from 14,156,515 shares (15.8%) as of Blackrock’s prior SC 13G/A filed February 4, 2020.

SC 13G/A filed by Vanguard (November 10, 2020)

Documents beneficial ownership of 4,062,203 shares (4.47% of shares outstanding), down from 9,584,043 shares (10.68%) as of Vanguard’s prior SC 13G/A filed February 4, 2020.

Initial SC 13G filed by Ameriprise Financial and various subsidiaries (November 10, 2020)

Documents new ownership of 10,972,057 shares (roughly 12.1%) of Newpark which partially offsets the 12,844,947 shares sold by Blackrock and Vanguard since February of this year.

Updated Financials: P&F Industries, Inc.

P&F Industries, Inc. reported financials for the quarter ending September 30 via Form 8-K filed on November 12, 2020. Revenues for the quarter were $12.4 million, down 16% as compared to the same period of 2019. We note that P&F Industries generated $1.8 million in quarterly cash from operations and spent $37,000 on capital expenditures, generating quarterly free cash flow of roughly $1.7 million.

P&F Industries’ unadjusted net current asset value as of September 30, 2020 was just over $17 million, or $5.38 per share, based on 3,151,060 shares outstanding. This unadjusted net current asset value is comprised of $908,000 in cash, $8.5 million in receivables, $19.5 million in inventories, and $1.8 million in prepaid expenses; less $9.7 million of current liabilities, $2.6 million in operating lease liabilities, $135,000 in other long-term liabilities, and a $1.1 million PPP loan.

II. AN OPEN CALL FOR READER ASSISTANCE

Originally published in D Magazine’s January-February 2011 issue, the excerpts below are today particularly timely in the co-editors’ eyes —

The Man Behind Crescent Real Estate Holdings

[John] Goff…draws four boxes to illustrate the different segments of his business life: Goff Capital Inc., Goff Capital Partners, Goff Family Foundation, and Crescent.

…Goff started working at the age of 12. He loved to make money—and he saved it. After earning an accounting degree at The University of Texas, he joined a CPA firm in Houston. He dove into the numbers, learning as much as he could about the financial operations of a business. Eighteen months later, he went to work for prolific Houston developer Kenneth Schnitzer. Then in 1981, the newly married Goff moved to Fort Worth, so his wife could be closer to her family. Goff had offers from a number of Dallas real estate firms, but opted to go back into public accounting and joined Peat Marwick (now KPMG).

“Something in my gut didn’t feel right about the real estate business at the time,” he says. “Within a few years, all of those firms I had talked with were gone.”

At Peat Marwick, Goff took on advisory work, audit work, SEC work, initial pulic offerings, soaking up knowledge and experience. He also connected with Richard Rainwater, the financial genius who grew a fortune—first for the Bass family, and then for himself.

After Rainwater left the Basses, Goff joined him. The then-32-year-old’s first assignment: take $50 million and buy companies that had been hit by the October 1987 stock market collapse. “It was frightening, but by this time I felt I could tear apart a financial statement as good as anybody,” Goff says. “I worked from the ground up, just trying to find companies that I liked that were being sold at what I felt were very cheap evaluations. It was nirvana for me.”

Quarterbacking Staubach

In the late 1980s, Rainwater and Goff were approached by Roger Staubach, who was looking to focus his growing real estate firm. At the time, The Staubach Co. was heavily invested in commercial properties. “Roger’s tenant rep business was quite small, but it was profitable,” Goff says. “We convinced him to focus exclusively on tenant rep, and we invested $1 million for a 20 percent stake in the company.”

That $1 million eventually turned into more than $70 million, through distributions and the $700 million sale to Jones Lang LaSalle in 2008.

“So many times the focus is on Roger and football, but he grew an incredible business,” Goff says.

Staubach shares credit for his firm’s success with Goff. “John was very instrumental in some of the decisions we made through the years—Richard, too,” Staubach says. “John is very smart financially and has a sense for people. He helped me develop a concept to grow the company without accumulating a lot of debt.”

Serving on The Staubach Co. board, Goff saw the beginning of what would become a significant migration of companies from the coasts into North Texas. At the time, though, Dallas was the most overbuilt market in the U.S.

“I went to Richard [Rainwater] and told him I wanted to take everything that was on my desk and set it aside and focus on the commercial real estate business,” Goff says. “I thought it was a chance for me to start my own company. He said, ‘Great, you put up your entire net worth.’ He then came up with what he was willing to expose to it—it was significant.” (Reports had Goff investing $8 million and Rainwater backing it with $110 million.)

“There was not one real estate professional in the area who thought it was a good idea,” Goff says. “But I felt in my gut that it was the right time to do it, as long as we could buy great assets at a discount to what they were built for.”

Building a Reit

During winter months, when he’s not in Texas, Goff can often be found schussing down the slopes at Beaver Creek in Colorado. He loves to ski fast, and he’s good at it, having raced as part of a Celebrity Pro-Am program several times. When he works out, he needs to be working toward something, he says. Racing through a giant slalom course helps him do just that.

Goff put that same drive and purpose into building Crescent. He began by lining up partners to invest in the various acquisitions. The first was Caroline Rose Hunt, who was looking to recapitalize The Crescent, a 1.3 million-square-foot luxury office complex in Uptown. After that 50-50 partnership was created, Goff put together additional buys, focusing exclusively on Class A buildings. He also took advantage of the real estate downturn to bring top leasing talent on board.

“I’d love to say it was easy, but it was really hard,” Goff says. “It took a number of years for the assets to turn around, to fill them up and validate that we bought at the right price at the right time.”

In May 1994, Goff raised more cash by taking the company public with a $550 million IPO. It was at this point that the venture was given a name—Crescent Real Estate Equities, in honor of Goff’s first buy and favorite property.

Thirteen years later, Crescent, which had become one of the largest real estate investment trusts in the country, was sold to Morgan Stanley for $6.5 billion. Investors who got in at the IPO were rewarded with a 15.4 percent compounded internal rate of return, including more than $3 billion in cash distributions.

“We were at a point where I felt prices had peaked,” Goff says. “I’m not about to say that I was smart enough to see what was about to come. It was just my gut, again.”

Crescent, Round Two

Goff turned his focus to Goff Capital Partners in 2008, buying up more than $4 billion in distressed real estate debt and growing his team. But by the summer of 2009, rumors began to swirl that Morgan Stanley would be giving up Crescent to lender Barclays Capital, which had a $2 billion note coming due.

Goff wanted back in. He tried to buy the whole thing on his own, but the parties could not come to an agreement on price. “What we were able to do was agree on a joint arrangement, so [Barclays] was able to stay in the deal and achieve upside along with me,” he says.

Barclays and Goff Capital Inc. formed Crescent Real Estate Holdings to acquire the Crescent portfolio in November 2009. At the helm again, Goff brought back five former Crescent executives—including John Zogg, managing director of leasing—and went about stabilizing and improving the assets. Along with five resorts, Crescent owns 35 Class A office buildings totaling 17.3 million square feet in Dallas, Fort Worth, Houston, Las Vegas, and Denver.

Goff scoffs at speculation that he is just repositioning the prized assets for sale. “These are not workouts; we are not interested in selling,” he says. “We are actually looking to grow the business, and have already committed a significant amount of capital to new projects.”

Goff’s gut is telling him 2011 will be a great time to buy. And he intends to listen. It hasn’t let him down yet.

Fast forward to 2020 —

Goff is a major shareholder of Contango Oil & Gas Company, holding 23.5% of shares outstanding as of his latest SC 13D/A (Amendment No. 10), filed October 27, 2020, per the merger of Contango Oil & Gas Company and Mid-Con Energy Partners announced on October 26, 2020.

In the words of Contango’s Chief Executive Officer, Wilkie Colyer —

This merger is exactly the type of transaction we look for to enhance value for our shareholders in the current market. We were able to substantially increase our reserve base and cash flow in an accretive transaction while meeting the needs of Mid-Con unitholders by further rationalizing their cost structure and mitigating their refinancing risk by combining our respective credit facilities…This transaction is simply the next step, and certainly not our last, in our stated goal of consolidating a sector that is in dire need of it. This combination increases our exposure to long lived oil reserves and is accretive to Contango shareholders. Our definition of accretive, by the way, is that it increases the intrinsic value of Contango on a per share basis, and this transaction certainly fits that bill. It also benefits Mid-Con’s unitholders by offering them enhanced liquidity, financial stability and opportunities for growth on a larger platform. We welcome Mid-Con lenders, unitholders, and employees into the Contango family. (October 26, 2020)

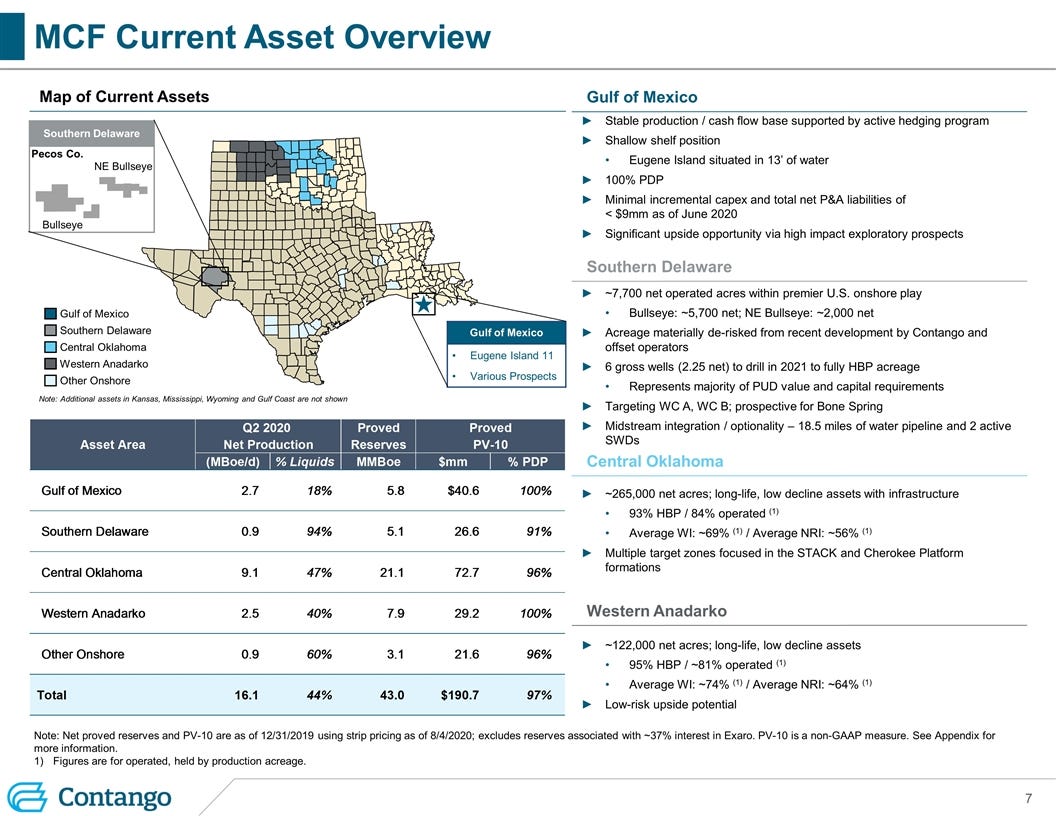

As detailed in a “Contango & MCEP Strategic Merger Presentation” filed with the Securities and Exchange Commission —

In addition to co-authoring this digest, the co-editors oversee the allocation of private family capital and are exploring an internal investment into the (post-merger) combined MCF/MCEP equity. The co-editors actively seek private dialogue with any Grahamian Value readers with oil and gas industry specialization and/or above situation-specific familiarity (and a shared willingness to compare notes) —

Harry Sauers: hsauers5@gmail.com

Shai Dardashti: shaidardashti@gmail.com

III. FEATURED GUEST INSIGHT

A thoughtful perspective on Hunting PLC, courtesy of Nothing But Net-Nets (twitter) —

Hunting: An Oil Net-Net (November 9, 2020): When scrounging around for cigar butts, it is rare to find one that is covered by Wall Street. Hunting PLC, a supplier to the oil & gas industry, is one of these companies. Despite the research coverage, Hunting still trades below net working capital. Such is the revulsion to oil stocks today…Hunting holds a fair amount of inventory and should generate a significant amount of cash as the business contracts. In this way, the business is counter cyclical. Working capital will unwind as revenues decline. Management seems capable and properly incentivized. They will continue to do tuck-in acquisitions. And most likely, they will stay focused on upstream oil and gas.

In the company’s own words —

We manufacture premium, high end downhole metal tools and components required to extract hydrocarbons across the well construction, completion and intervention stages of the well's lifecycle. Through the development of our own technologies and proprietary know-how we are well positioned to secure market share by protecting our intellectual property by means of patents and trademarks. Hunting's substantial IP portfolio is a significant barrier to entry for competitors and allows us to defend margins and offer more operational flexibility, particularly in a downturn. The Company's broad range of products and associated services spans the lifecycle of the wellbore, irrespective of whether it is intended for oil, gas, onshore or offshore, conventional or unconventional. We manufacture premium, high end tools and components required to extract hydrocarbons across the lifecycle of an oil and gas well. A distinguishing feature of the Hunting product offering is the ability to manufacture high tolerance products. (source)

IV. WEEKEND WATCHING

Courtesy of McCombs School of Business at University of Texas at Austin: Keynote interview with John Goff, BBA '77, and Dean Jay Hartzell at the Alumni Business Conference in Rowling Hall. (Recorded September 20, 2019)

Courtesy of Stanford Graduate School of Business: A tribute video created by Richard E. Rainwater's daughter, Courtney Rainwater, and her friends at Trinity Films. The video gives a richer insight into what makes Richard a very special person. Rainwater, MBA 1968, was the 2010 recipient of the Arbuckle Award, presented by the Stanford Graduate School of Business. (Recorded February 2010)

V. WEEKEND LISTENING

Courtesy of The Tim Ferriss Show, hosted by Tim Ferriss (twitter): In this episode, we have Peter Attia interviewing Sam Zell, a legendary dealmaker and investor. Sam is the Chairman of Equity Group Investments, and he was recognized by Forbes as one of the “100 Greatest Living Business Minds” in 2017. He holds a place on New York Stock Exchange’s “Wall of Innovators” for his role in building the $1 trillion REIT industry. Sam is also the author of Am I Being Too Subtle?: Straight Talk From a Business Rebel. (January 23, 2020 episode date)

Courtesy of Invest Like the Best, hosted by Patrick O’Shaughnessy (twitter): Jeremy Grantham is the co-founder and chief investment strategist of Grantham, Mayo, & van Otterloo (aka GMO). GMO, which manages more than $60B for clients, was a firm that helped educate me early in my investing career. They’ve long published thought-provoking research, most of which came from Grantham himself. He is regarded as a highly knowledgeable investor in various stock, bond, and commodity markets, but is particularly noted for his prediction of various bubbles. In this conversation we discuss the current crisis, which he calls the fourth major event of his long and storied career as an investor. As he says, this one is the most uncertain. We also discuss unique topics like commodity-based companies, and how opportunity often lies between fields of expertise. (June 9, 2020 episode date)

Courtesy of This Week in Intelligent Investing, hosted by John Mihaljevic (twitter): Phil Ordway of Anabatic Investment Partners takes a look at some of the more excessive equity-based compensation practices at public companies, particularly in the tech sector, and how they may dilute long-term investors’ returns…Elliot Turner of RGA Investment Advisers explains how he uses so-called “reverse” discounted cash flow (DCF) models in order to isolate the key variables that drive a company's valuation. One of Elliot's preferred analytical tools, reverse DCFs enable him to assess market-implied expectations and to develop a high-conviction variant thesis. (November 7, 2020 episode date)

ABOUT GRAHAMIAN VALUE

Founded in 2020, Grahamian Value is a labor of love centered around our desire to openly share data and perspectives that we find helpful in our pursuit of Benjamin Graham-inspired investment ideas.

The co-editors of Grahamian Value, as of the date of this communication, may individually own shares of companies mentioned herein. The publishers do not receive compensation from the companies and people covered in Grahamian Value for such coverage. This communication is for informational purposes only. This is not intended to be investment advice. Seek a duly licensed professional for investment advice.